Pools Are Not Commercial Services

Regional public pools are not designed to operate on a commercial basis. They are subsidised essential public infrastructure delivering:

- preventative health outcomes

- water safety and drowning prevention

- social connection and community wellbeing

- equitable access to recreation.

Profit and loss measures financial performance, but these community-based outcomes sit outside the revenue line.

Structural Cost/Revenue Imbalance

The business model for regional pools is inherently imbalanced:

- Revenue is constrained by small population catchments with limited preparedness to pay (affordability expectations).

- Costs are largely fixed, including staffing, compliance, maintenance and asset lifecycle costs.

- Depreciation dominates full cost, reflecting the capital intensity of service delivery.

Under these conditions, a negative operating result is structurally inevitable, regardless of management quality.

Profit and Loss Ignores Public Value

A Profit and Loss Statement captures income, expenses and the net financial result. It does not capture:

- avoided healthcare costs

- reduced drowning risk

- improved mental wellbeing

- equity of access

- community resilience.

This creates a distorted picture where a pool can appear “under-performing” financially while delivering net positive value to the community and broader public system. Many of the community benefits associated with utilisation of public pools accrue to state and federal budgets.

Misleading Comparisons and Perverse Incentives

Over-reliance on Profit and Loss can lead to:

- inappropriate benchmarking against metropolitan facilities

- pressure to increase fees (reducing access and participation)

- under-investment in maintenance (deferring cost)

- decisions that optimise short-term financial results at the expense of long-term outcomes.

In extreme cases, it can bias the council’s decision-making toward pool closure without fully considering lost public value.

Depreciation Distorts the Narrative

When depreciation is included:

- It often becomes the largest cost component, dwarfing everything else.

- It reflects future capital obligations, not current cash outflow.

While depreciation must be considered for long-term sustainability, using it as a measure can:

- overwhelm all other considerations

- obscure operational performance

- shift focus away from service outcomes.

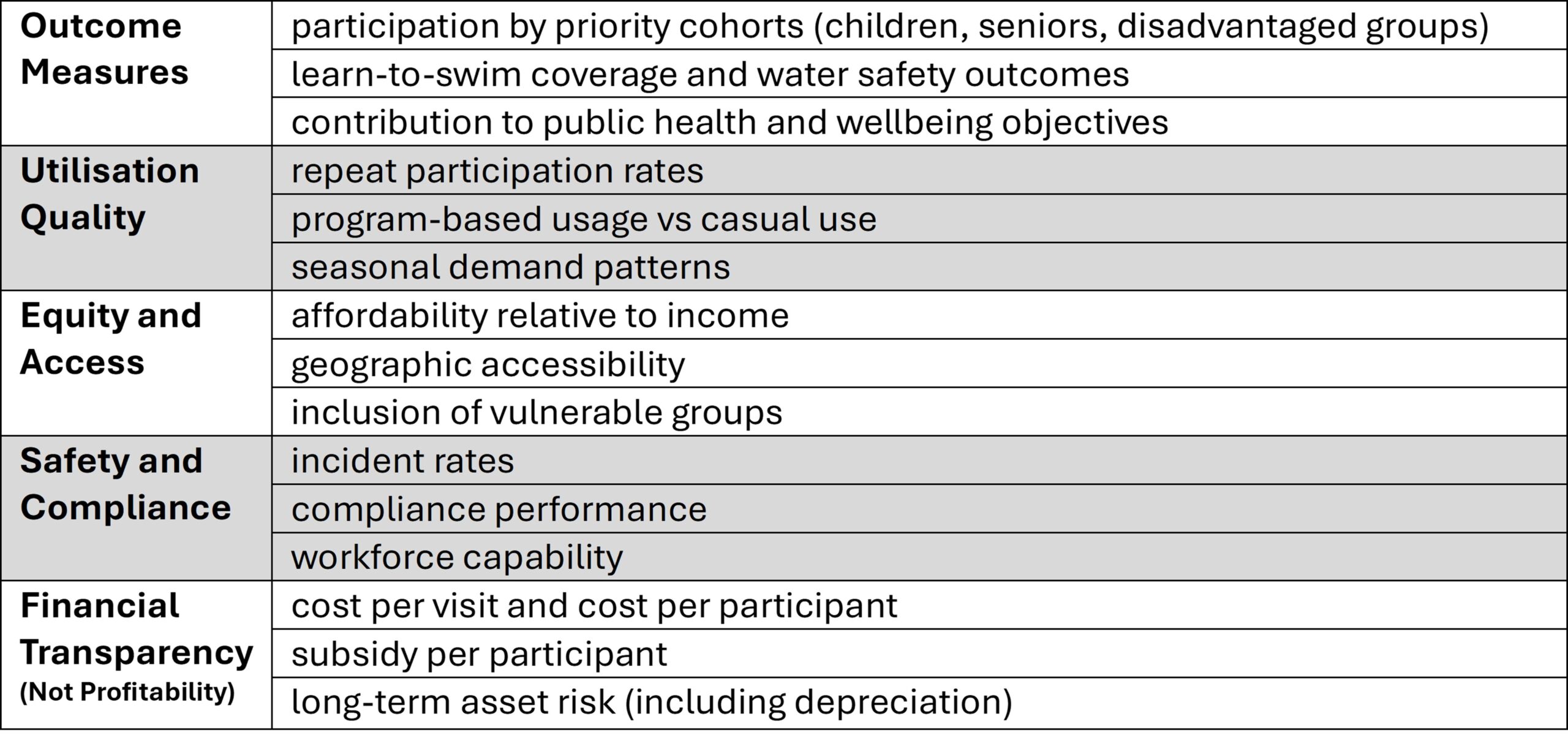

What Should be Measured?

Rather than relying on Profit and Loss alone, regional pool performance should be assessed using a multi-dimensional framework that includes:

This re-frames financial metrics as context, not the sole measure of success.

Regional public swimming pools should be evaluated based on

outcomes they deliver relative to the level of public subsidy required,

rather than their ability to generate a financial surplus.

Conclusion

Profit and Loss remains a useful reporting tool, but it is insufficient and potentially misleading as a primary performance indicator for regional and remote public pools. These facilities are better understood as public value assets, where success is defined by outcomes, access and risk management, supported by transparent financial metrics.

About Ravim RBC

Ravim RBC is a strategic consultancy assisting councils around Australia with service planning and conducting service reviews. Since 2014 our consultants have been shaping council services to align with community needs and expectations and preparedness to pay.

0 Comments